Author:ZeMing M. Gao, business strategist; IP attorney (USA); Company-as-a-Product (CaaP) expert; IP builder/strategist/economist; blockchain strategist/economist; tokenization and smart contracts expert; SEC/FINRA Investment Banking representative, Chief Advisor at Caapable.com advising multiple companies; email: gao@caapable.com

Highlights:

- Introduce Sharener, a socially networked business & consumer space (B&C Space) created in the general commercial space. The new B&C Space is sustained by a triangular and bidirectional strong “social force field” naturally emanating from stable and strongly-binding business and consumer activities.

- In the B&C Space, the consumer energy spent in the process of purchasing and consuming is effectively converted to a resource useful to the business, and the business in turn rewards the contributing consumer financially on a specific, purposeful and correlated basis, rather than using mere advertisements.

- The B&C Space includes several powerful interactive subspaces, including a C2C social space in addition to B2C and C2B commercial spaces.

- The integrated platform incorporates a personalized price function to assure the correlation between the flux of the force field and personal contribution.

- The financial rewards given by business to consumer are fulfilled in retail channels using an innovative virtual crediting system to complete the business-consumer feedback loop.

- The B&C Space enables truly integrated on-line and off-line shopping, and creates a new conductive and productive B2C direct sale business model.

- The B&C Space generates a new productive power which results in not only enhancement in business efficiency but also a commercial world that is more reasonable and more just and fai

Part I – THE BACKGROUND

An Introduction to the General Commercial Space

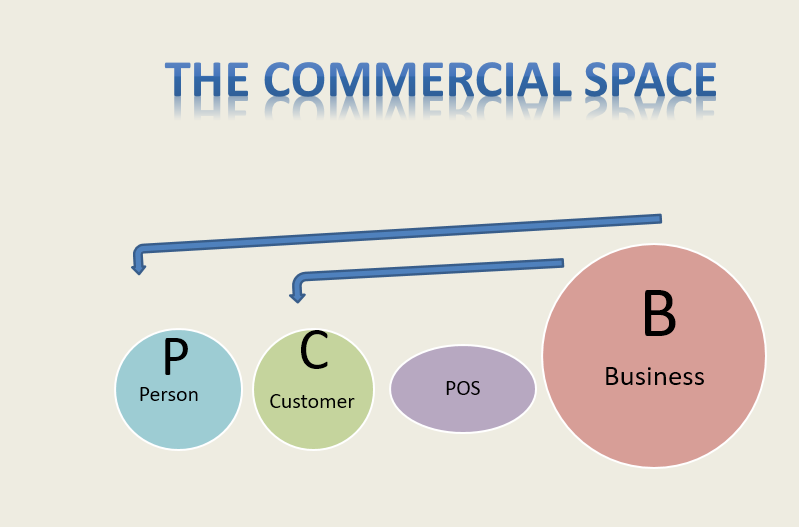

- In the commercial space, Business (B) reaches out to Customer (C) through advertisement and promotional means. (In this document, the word “customer” and the word “consumer” are used interchangeably, unless otherwise noted.)

- Typically, B and C connect through point-of-sale (POS).

- At the same time, business (B) reaches further out to people at large and try to convert Person (P) into Customer (C).

- The commercial space creates numerous possibilities of interaction between various entities, and when these interactions come together coherently to serve for a purpose, it forms a distinctive business model.

- There are several sub-spaces in the commercial space as follows.

The P2P Subspace

(person-to-person, or peer-to-peer)

Facebook – The biggest piece in the P2P space.

- Facebook takes a P2P form, but has not decided on its specific business model. Many have automatically assumed that the business model of Facebook is to be advertisement based, much like Google. But Facebook has been approaching this from a more cautious way, knowing that the P2P space it has occupied may be too valuable to be locked in an advertisement based model.

- In the P2P space, the business (B) is not an inherent part, rather a bystander trying to enter from outside to grab a piece of “P” (person) and convert it to “C” (consumer), thus creating a secondary B2C subspace from the P2P space.

- The vast P2P space is regarded as the largest piece of remaining territory in the e-commerce space. Facebook is already valued at above $50 billion although it does not have a clear business model yet. However, it is unclear how much of the P2P space can be converted to profitable B2C subspace.

RenRen.com – The closest Chinese counterpart of Facebook in the space of P2P.

- Recently went public with a valuation of 7.5B. Unlike Facebook, RenRen.com took the advertisement-based approach.

- By the Facebook standard, there is really no real P2P in China. Internet portals (such as QQ.com), forums, blogs and mini blogs (Weibo) in China really have not formed extensive P2P. The connectivity level is simply not there when compared to Facebook. Chinese P2P sites have only remote, simple and temporary single lines of social contact, but have not formed tight, sophisticated and permanent social spheres. In essence, the sites belong to the category of communication tools, instead of real net-societies or social networking space, as the depth, extent and stickiness of “social networking” is far below that of Facebook.

The B2B Subspace

(business-to-business)

Alibaba.com – Possibly the biggest B2B site on the Internet.

- In the US, B2B did not take the route of public Internet. Instead, B2B in the US grew naturally based on the interaction among the existing businesses. The B2B commerce activities in the US are much deeper and sophisticated, but do not have a broad public Internet platform like Alibaba.com. Instead, they tend to take separate connections between companies that already do business with each other. One example is the specialty vertical market B2B networks. In other words, B2B in the US is narrow but deep, while B2B in China is broad but shallow.

- However, Alibaba is expanding and deepening its platform hoping to make it both broad and deep. If successful, it would have some large implications.

The C2C Subspace

(customer-to-customer, or consumer-to-consumer)

eBay – the most commercially successful C2C. However, eBay is quickly being transformed to a B2C platform.

- com in China started as a competitor of eBay, but it was mostly B2C from the very beginning, with very little C2C content.

- We believe that C2C is not a prime business model in the commercial space. It is fundamentally a secondary concept. Clearly eBay itself is fully aware of this shortcoming.

The B2C subspace

(business-to-customer)

- Amazon

- com

- eBay

- And countless e-commerce websites.

- In fact, if it is not limited to e-commerce,B2C essentially encompasses the vast majority of the entire commercial universe.

The C2B Subspace

(customer-to-business)

- C2B business model is relatively novel

- In the most common forms of C2B, customer (C) offers a service to business (B) and gets paid by business. It is a reversal of traditional B2C business model. Examples are blogs or internet forums where the author offers a link back to an online business facilitating the purchase of some product, and the author receives affiliate revenue from a successful sale.

- Under this model, C is really not a customer in a strict sense, but rather like a temporary independent contract worker. So this is better called b2B, rather than C2B. These are only single-line connections based on direct economic benefits of a more casual type of “employment”, not actual social effects of a real B&C society.

- Besides, the above model has not achieved any scale, far less than forming a B&C commercial space.

Blippy C2B model:

- Blippy is free site that lets one share purchases and see what friends are buying online and in real life. Blippy lets you communicate about and share purchases with friends by syncing already existing e-commerce accounts to Blippy such as iTunes, Netflix, Woot, eBay and more.

- This model starts to show some real C2B element, as it has some social sharing effect among C and C.

- Blippy takes the traditional advertisement-based business model. Overall, the commercial space formed by Blippy is incomplete. First, it has not formed a complete feedback loop between C2B and B2C, let alone concrete means to facilitate the commercialization of the space having such feedback loop. Second, the “force” that sustains the space is just curiosity (as many like to volunteer on writing reviews and comments for enjoyment only). This is not a full scale normal commercial force, and has limited structural reach.

Groupon

- An aggressive C2B business model

- Groupon created a unique C2B space in the e-commerce space. Perhaps even Groupon itself does not realize the fact it operates in the C2B space. In the C2B space, the business is initiated by consumers and directed to businesses. Although the end transaction in Groupon deals is still one from B to C as in the regular B2C space, the Groupon business model itself is distinctively C2B.

- However, as will be explained below, there is something fundamentally wrong with Groupon’s business model.

The Groupon Defect

Groupon serves to profit on consumers’ desire for “good deals”, but unfortunately has only an effect of taking advantage of others. The force field that sustains this business model is businesses’ fear, ignorance or curiosity at best.

Groupon platform does not provide a mechanism to form natural group purchases. Rather it is an alliance based on artificial promotion at a cost of damaging existing business relationships and destroying long-term business opportunities. In commercial space, this is not a normal business alliance, but rather akin to gang robbery. On one hand, it robs the businesses, but on the other hand it also robs the other regular consumers, especially the royal customers of businesses. The actual robber is the organizer of the group purchases, not the purchasing group.

With Groupon, there is no win-win synergy, but only win-loss dichotomy. In the real world, win-win cannot be supported by mere subjective goodwill, but requires physical support by real synergy based on extra productive energy generated by a business model. The business model of Groupon does not contribute productive energy to the society. It may seem to help increase the retail efficiency, but this is only an illusion, which happens only because no other method exists to substitute the defective Groupon model.

Other related services

- Google Places

- Google Offers

- Foursquare

- Gowalla

- Yelp

- AStoreNearMe – has a division OfferIQ just sold to Transactis. Similar to how consumers are targeted online through their Internet shopping patterns, OfferIQ tracks and targets the movement of consumer’s offline shopping habits using a special credit card payment system which links off-line shopping to the online membership-based advertisement.

PART II – The New B&C Space

Disclosed herein are a novel integrated customer-business space and business platforms and methods derived from the new commercial space.

The invention creates what is missing among the existing commercial space:

- a B&C Space, which is a business-consumer social networking space forming a natural, correlated, and interactive a C2C, B2C and C2B society;

- a B&C Space sustained by a triangular and bidirectional force field which includes both C2C social attractions and B2C and C2B financial attractions;

- an integrated fulfillment system to financially fulfill the consumer benefits in both online retail and offline retail; and

- an integrated advertisement system that not only conducts targeted online advertisement, but also correlatively interacts with consumers offline.

A. B&C Space – function and purpose

- B&C Space is a revolutionary integration of commercial space and consumer space to fundamentally improve the overall efficiency of the commerce and consumer channels.

- B&C Space converts the consumer energy spent on the process of purchasing and consuming to a resource useful to the businesses, and allows the businesses to in turn reward the contributing consumer on a specific, purposeful and correlated basis, rather than using mere advertisements.

- B&C Space uses personalized price function incorporated in an integrated platform to assure the correlation between the flux of the force field and personal contribution.

- B&C Space creates a new production power to result in not only efficiency enhancement but also a more reasonable and more just and fair commercial world.

- B&C Space may include not only the Internet, but also includes a mobile consumer network and a widespread retail network (both online and offline), and may further integrate “The Internet of Things”.

- B&C Space is sustained by a force of natural attraction, instead of forces of coercion or allurement.

B. B&C Space – its Force Field

B.1. Force fields in commercial space in general

Why introduce the concept of force field into commercial space? It is because the force field is the key. A vague and general concept of a B&C Space is not new. But what matters is not a mere concept and a name for it, but the structure and the characteristic physics that governs the space.

In defining and realizing a commercial subspace, it is of fundamental importance to understand the following:

(1) The purpose and functions for its existence, including both commercial functions and social functions.

(2) Exactly what force field sustains the subspace?

Understanding the B&C Space requires firstly an understanding of the existence of a C2B subspace, its function and sustaining force field, and how the C2B subspace relates to the existing B2C space.

Although many elements of the B&C Space already exist, seeing the systematic and structural aspect of an integrated B&C Space and coming up with an architectural plan to build the space is pioneering and may lead to a revolution.

B.2. Force fields in exemplary commercial subspaces

The function of a commercial subspace and its sustaining force field may be understood using the several existing commercial spaces as examples:

- P2P – Its function is to communicate, while its sustaining force field is a growing need for social connection and feedback. The success of Facebook has proven that this is a very strong force field. However, this force field is not inherently commercial and does not naturally and directly apply to business. What can be commercialized is really a peripheral “radiation” of this strong force field through much manipulation.

- B2B – Its function is to facilitate trading, while its sustaining force field is a mutual need for maintaining a business relationship. Even though there is potentially a strong force field to sustain a B2B space, the current B2B platforms such as Alibaba.com have established only a very weak force field, which is essentially a need for introductory business information and little more. The resultant business relationship results in no strong affinity nor long-term loyalty. It also lacks mutual feedback.

- C2C – The function of the existing C2C is to supplement the B2C space. C2C provides a commercial channel for “secondary goods” (used products or products that have fallen off the regular marketing channel). Therefore, the sustaining force field of the C2C space results from the need for frugality of consumers (and occasionally a need for unique products). This is not a very strong force field, and further has a relatively small radiation surface. However, as described herein, the disclosed new B&C Space includes a very powerful C2C space (in addition to B2C and C2B spaces) in which C2C is a socially networked like P2P, but at the same time inherently related to businesses and individuals participate the B&C space as a consumer (C), not a mere person (P).

- B2C – Traditional B2C encompasses the main body of world commerce, and is not the subject of the current discussion. Innovative B2C business models like Amazon.com serve the purpose of creating important “longtail markets”, while the sustaining force field of these B2C spaces are the need for convenience and product selectivity.

- C2B – So far, there has not been a good business model for C2B. The most prominent C2B model Groupon has an inherent defect (see more discussion below).

B.3. The Force Field of the B&C Space

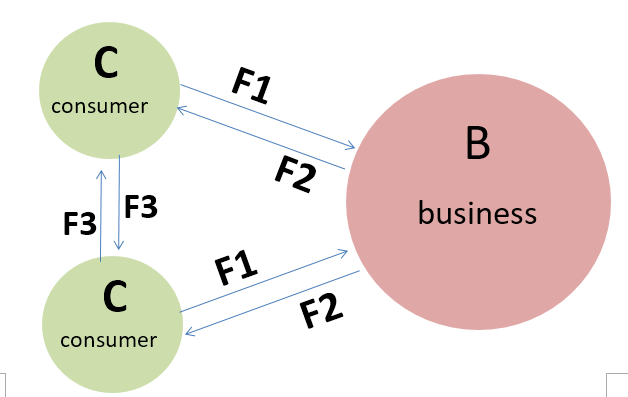

In contrast, the new B&C Space is an integrated commercial space sustained by a triangular and bidirectional strong force field:

- B&C Space is sustained by a force of natural attraction, rather than coercion or allurement

- Force F1 is an attraction force going from consumer to business (C2B, where C attracts B) , contributed and measured by:

(1) customer loyalty;

(2) active customer contribution such as product-specific information C2B feedback and C2C discussion.

- Force F2 is an attraction force going from business to consumer (B2C, where B attracts C), embodied in:

(1) Highly personalized and effective product information deliverance (versus harassing advertisements)

(2) Personalized pricing with discounts or credits (fulfilled through an integrated fulfillment system such as the inventive virtual crediting system disclosed herein)

- Force F3 is a C2C motivating force that exists in the socially networked community.

- F1, F2 and F3 are interdependent on each other. Between a particular pair of B and C, F2 increases as F1 increases (greater reward given to greater contribution). At the same time, naturally F1 may also increase as a response to a greater F1, while F1 also increases due to greater F3 which corresponds to a greater social stimulus. In an ideal state, the force fields in the B&C Space should achieve a dynamic equilibrium.

- B&C Space provides a platform to connect consumers and businesses through both the B&C platform and retailing points and form a medium which propagates the force field.

- Triangular and bidirectional strong force field (C2B, B2B and C2C) sustains a stable and strongly-binding social force field generating high energies.

- In the B&C Space, the consumer energy is excited (motivated) by a two-fold source. One is financial reward from business (B2C), the other social reward from the C2C social networking. These are forces of natural attraction, rather than forces of coercion or allurement.

- The integrated platform assures the correlation between the flux of the force field and personal contribution.

- The result is a new productive power to result in not only an efficiency enhancement but also a more reasonable and more just and fair commercial world.

C. Personalized Price Function in B&C Space

In the B&C Space, personalized pricing is the most important form of personalized incentive in the C-B relationship

- For a given product, its price p is a variable, which is a multi-variable function (pricing function):

p = F(p0, lr, cr, sa, pa) - where p0 is base price, lr, cr, sa, and pa are personalized parameters, representing loyalty reward, contribution reward, social adjustment, and promotional award, respectively.

- The pricing function determines a personalized price according to the several personalized parameters, which themselves may be calculated using score functions or ranking functions respectively. These personalized parameters may have different degrees of personalization. Some may only vary from individual to individual, but remain a constant for all products for a given individual, while some may vary not only from individual to individual, but also from product to product for a given individual.

- The pricing function needs not be a continuous or smooth functioning, or an analytical function. It may be determined using any practical model or pattern. The core is that when the personalized parameters change, the price changed accordingly.

- It is a nontrivial matter to implement a retail method to actually incorporate personalized prices which varies from customer to customer for a given product. For example, using the conventional retail system and payment system, it may not be possible to implement a continuous and smooth personal price function.

- However, a great deal of personalization in pricing may be realized using methods that are easy to understand and easy to carry out without requiring a smooth price function. A virtual credit system as described herein is an example.

- In the future, however, if an automatic personalized payment system is integrated into the B&C Space, the price function may approach smoothness.

It is noted that personal price function may be replaced by a personal discount function, a personal reward function, a personal credit function, etc., all to the effect of achieving a price of a product that varies from individual consumer to individual consumer.

PART III – B&C Platform

B&C Platform is a commercial embodiment of B&C Space.

A. An overview

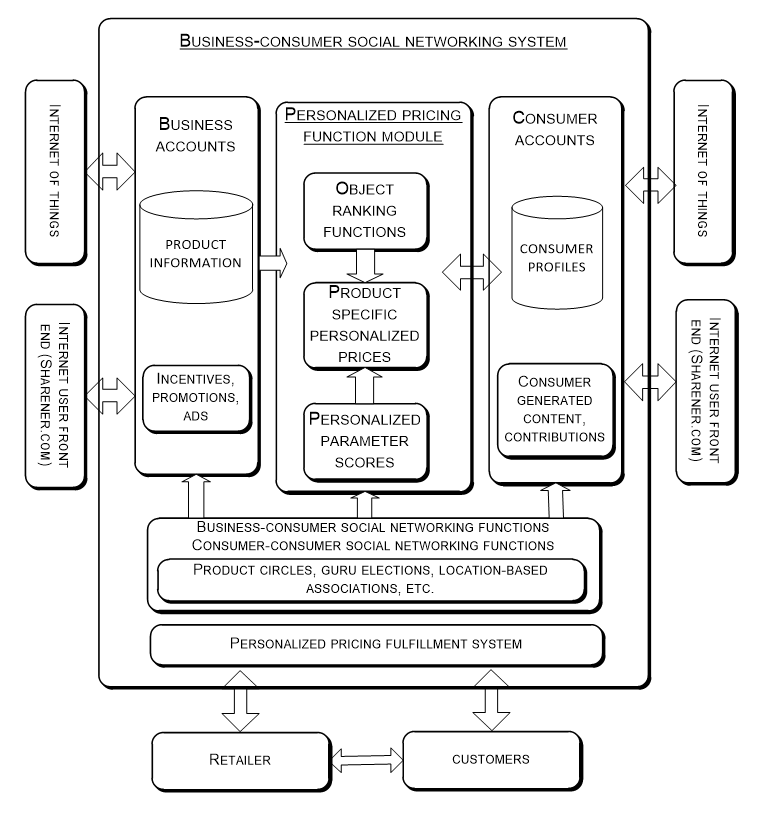

B&C Platform is a business-consumer social networking system.

The core of B&C Platform is a server-based system hosting interactive business accounts and consumer accounts. The business accounts including product information, incentives promotions and ads, are connected with consumer accounts through a personalized pricing function module. The personalized pricing function module ranks various objects is an object ranking functions. The ranked objects may range from separate user inputs (such as user product reviews, comments and feedback) to each consumer as a whole. These ranking functions form a basis for calculating product-specific personalized prices for each consumer.

The B&C Platform has a server-based backend, and may have multiple frontends. One primary front end is a social networking website to provide Internet-based user interface with business users and consumer users. The user interface may be browser-based, but may also be application program based (such as a mobile app).

Another frontend provides a communication port for retailers and consumers to communicate purchase-related information to the server-based backend. This frontend may be Internet-based but may also be any other communication channel (such as mobile communications) and may or may not have a browser-based user interface.

Sharener.com is the domain name of the B&C social networking website. The website may be different from the common B2C websites such as amazon.com and taobao.com which list a large number of products for sale. Instead, the website primarily features social networking functions to connect consumers to products and businesses. The website embodies a society “where a loyal buyer is a business partner, and every discount is personally deserved”.

The website has two distinctive user registration panels, one for consumers and the other for businesses.

Upon registration, a consumer may have access to unearned coupons as a starter.

The central attraction of the system, however, is that each consumer develops a personal collaboration relationship with the products and businesses he may be interested in and receives both financial and social rewards.

The system accumulates a set of personalized characteristic information for each consumer. Such characteristic information may include purchase history, feedbacks given by the consumer, and responses by business and other consumers to the feedbacks. The characteristic information collectively determines what credits (or other incentives) the consumer is to be given for purchasing the related products, as reflected in the personalized pricing model. Accordingly, the actual purchase price of the consumer would be a function of multiple variables. The function does not need to be a continuous and smooth function.

Behind the central website is a large-scale database and server systems providing data management and analysis of mass user information to support creation, delivery and management of coupons, rebates and credits (collectively called “credits” herein).

The consumer is not required to purchase product at the central website with the credit offered in order to fulfill the credit. The website may only support user registration and social networking between consumers and businesses, and allows the consumer to fulfill the credit in an appropriate retail channel.

With the credit offered, the consumer may go to a retail point of his choice to fulfill the credit (e.g., to redeem a coupon). In one embodiment, the retail point may be any place that sells the product and is not required to be associated with the central website in order to fulfill the credit. Instead, the credit is fulfilled by the central website through a novel self-governed redemption process, leaving the retail entirely outside of the loop. In another embodiment, the retail point is networked with the central website for coupon redemption.

For example, in one embodiment, the consumer purchases the product by following a link to another e-commerce website selling the product.

But more importantly, the consumer credit received at the central website may be fulfilled in a purchase made at any off-line or online retail point which may be unrelated to the central website.

In one embodiment, the credit fulfillment is completed by the consumer using a mobile phone whose number is registered with the central website and is associated with the consumer. Sharener therefore works hand-in-hand with the mobile coupon system.

The real ID-based membership and society has an inherent deterrence against fraud. Frauds may be further deterred by selective auditing and the social and economic forces inherent in the social network on central website.

Sharener therefore has two essential elements:

(1) the creation and maintenance of personalized B-C relationships (including a feedback loop between B and C) and use them as a basis for personalized rewards (e.g., credits through personalized pricing); and

(2) the facilitation of convenient and systematic methods to fulfill (materialize) the received reward through a purchase.

- Coupons, rebates and credits are several exemplary means for fulfilling a financial reward. Each of these methods, in their traditional meaning, places the burden of risk on a different party. Coupons place the risk on retailer, rebates place the risk the consumer, while the credit places the risk on the credit issuer (very often the manufacturer). Different risk allocation may require different redemption process and payment process.

- Although Sharener may use coupons, rebates and credits in the traditional sense, we introduce, in one embodiment, a virtual credit system to ensure a more balanced risk distribution and a more convenient redemption process. The virtual credit system works in reverse to the virtual payment system used in some existing commercial payment systems such as AliPay.

B. The Reciprocal Ranking on the B&C Platform

One key function of the B&C platform is reciprocal ranking of consumers by businesses or the platform. While a consumer ranks of business and product by studying, reviewing, commenting and purchasing the product, the business in turn ranks the consumer for the consumer’s “customer value” based on the consumer participation and provides a personalized incentive to the consumer. As illustrated herein, one way to provide personalized incentive is to give a personalized discount for purchasing the product or other products of the business. This may be done using a personalized price function to determine a price that is different from the consumer to consumer according to the ranking of the consumer (see “C. Personalized Price Function in B&C Space” in PART 2, and further discussions below).

Each consumer may have different rankings with regard to different businesses, and further with regard to different products or different product categories. The ranking may be done using the ranking functions provided by the platform, or by customized ranking functions provided by the business.

C. Personal characteristic information on the B&C platform

Regardless of which form (coupons, rebates, credits or virtual credit) is used, personalized pricing requires personal characteristic information, its creation, storage, management, usage and verification.

In addition to identifying each consumer, personalized characteristic information is also the basis to determine the personalized price. For a given product, its price offered to certain customer is a multi-variable function (pricing function) of both the base price personalized parameters such as loyalty reward, contribution reward, social adjustment, and promotional award, respectively. The personalized parameters themselves may be calculated using score functions or ranking functions respectively.

Where the personal identification information is stored may not be a major technical problem, but it is critical to the business model. This is in fact a major battlefield among mobile carriers (e.g., AT&T), hardware manufacturers (Apple, Nokia) and Internet service providers (Google, Apple)

Most personal characteristic information may be stored on the server of Sharener, but certain personal identity information may be stored in any of the following places:

- SIM card of a mobile phone,

- Mobile phone memory

- A personal account held at Sharener

Depending on how the personal identification information is stored, different operation methods and collaboration modes may be applicable. Sharener.com has flexibility in accommodating various needs.

D. The Social Nature of Sharener

The consumer participation in the business-consumer social networking platform is not only financially rewarding to consumers, but is also socially rewarding.

With regard to the connection between each consumer and various products, one or few customers may be elected to a “guru status” which signifies an honorable status of being an expert or leader (chief or mayor) of a certain product or brand. The “guru status” is designated officially on the platform and recognized either universally or locally.

The “guru status” may be determined using a set of ranking functions and/or score functions. The status may be dynamically adjusted.

Product gurus may enjoy not only recognition, but also significant financial rewards. It is conceivable that certain business may be willing to offer certain product for free to the relevant gurus.

In addition, the existence of product gurus may significantly help other consumers who need information on a product. Consumers may make the guru as the first stop for product information before making a purchase decision, much like going to a city mayor’s office for local information.

Sharener provides initial incentives for beginners to start, but has a snowballing effect and viral effect to result in exponentially increasing social and economic adhesion due to the social nature of the B&C platform.

E. Naturalness of the Relationship in Sharener

A high level of personalization between business and customer may have existed in the ancient personal businesses which had an inherent mechanism for rewarding personal relationship in business. But industrialization has all but destroyed that personal aspect in business, and led to the current situation where not only does personal participation of the consumer fail to occur systematically in a multi-business multi-channel business world, but also lack in even single business-consumer relationships.

Sharener brings back this natural personal factor to the commerce world, but to a much higher level. Technology once caused impersonal separation, but better technology makes it good again and even better. This is revolutionary.

Sharener is enabled by the technological advancements including: (1) the ability to connect a large group of people in a triangular and bidirectional network; and (2) dramatically decreased cost of enabling technology

A sharener is more than just a sharer. A sharener shares and gets rewarded in the Sharener society.

It’s a new society in which virtues like loyalty, friendliness, and wisdom are shared with your favorite businesses, and economically rewarded – instantly and personally.

In this new society, no one is a busybody and everyone is a business-buddy; and companies reward people’s goodness, but are at the same time not afraid of destructive forces like gang-up group coupons forced upon by an unrelated middleman organizing strangers who make no positive contribution to the business.

F. High-level Custom Participation in business on Sharener

On Sharener.com, businesses and consumers join the platform to form a society sharing resources. Unlike that found in traditional business-consumer associations, business joins Sharener in a very high degree on Sharener.com.

Conceptually, the level of participation by a business and a consumer in an online platform may happen in various degrees:

- Level 1 is the most passive form of joining, which is to just let the search engine find the business information such as a regular website.

- Level 2 creates special weblets in targeted format (like that in the Google Places) on a special platform (such as a location-based service) so the weblet of the business shows highly relevant information and appearance when a user finds the business.

- Level 3 creates user accounts for businesses on the platform for tighter information correlation and management.

- Level 4 allows business to reach out to customers actively through the platform instead of just passively waiting customers to come.

- Level 5 closely associates business with customers by providing personal incentives such that the customer becomes a business partner.

- Level 6 establishes a credit-fulfillment system in connection to a payment system to materialize the personal incentives awarded to the customers.

- Level 7 uses the result of Sharenology including social statistics derived from B&C Space of Sharener to dynamically optimize the business relationships in the B&C Space.

In Sharener, the level of participation is at least Level 4, and preferably Level 5 or above.

Sharener creates an extended virtual existence of a business by using customer participation and feedback. Starting with the basic information provided by the real business itself, Sharener adds user content based on customer participation and feedback, including products bought, services used, experiences, images, videos etc. to create an extended lecture existence of the business. The consumer space is no longer a mere target of the business, but instead an integral part of the business.

G. Sharenology

As Sharener platform accumulates business and user data, it forms a rich database of personalized business information.

The database forms the basis for a new science called Sharenology (science of shared business energy). Sharener shall lead in the study and applications of sharenology.

The core of Sharenology is the study of the optimization and applications of personalized price functions.

Sharenology is the theoretical basis of the business model of Sharener.com. For example, Sharener.com needs a personalized price function as a key link between each business and its consumers. The price function is a multi-variable function, and may have different levels of precision (resolution), ranging from a rough multi-staged tier setting to a continuous smooth price function. The price function may be customized for each business (e.g., using different combinations of the variables or parameters).

H. Sharener’s Revenue Model

Sharener may but does not have to use the ad-based revenue model. If it does use ads, the ads would be natural and relevant. The ads can be an integrated part of the direct B&C relationship to reach those who already have a recognized relationship with the business, or more broadly to reach others who may just have a potential for the business. Likewise, the ad may be made by a business that is already a part of the B&C society, or by any business that just has a general interest.

Sharener’s service may be multi-layered to let members enjoy certain basic benefits for free, and allow businesses to buy higher-end services. For example, basic business membership may enjoy free interaction with consumer members on Sharener, while premium membership may receive benefits such as personalized and targeted data, mobile coupon redemption, coupon clearance, and connection to Internet of Things.

Fees can be subscription based, or per transaction commission based.

I. Sharener’s revolutionary role in commerce

Sharener will cover the entire commerce world (both online and offline), and is the beginning of a whole new business regimen.

Prior art search has shown that the concept and the implementation of Sharener are novel and have many significant patentable aspects.

In contrast to the Sharener’s breakthrough concept, the existing B-C relationship is largely arbitrary and occurs at the peripheries of two different spaces (the business space and the consumer space). Other than the purchase itself, the consumer does not play an active role in the existing B-C relationship, and there is little feedback from the consumer outside of the purchase (pre-purchase or post-purchase), and there is less still (virtually nonexistent) response or reward from the business to the consumer. In other words, the business space (where the development and the production of products occur) and the consumer space (where the study, selection, purchase and consumption occur) do not have any significant integration and interaction in the existing B-C relationship.

Sharener defines a new interactive B&C Space in which the consumer behavior is, for the first time, no longer an act that occurs in a world separate from the business world, but rather an integral part of it. The consumer behavior, including not only the purchasing but also the pre-purchase and post-purchase behavior, is directed to the commercial channel to become an integral part of the commerce.

The B&C relationship is interactive and has a real feedback loop, and is further personalized, with specificity down to the individual level.

The personalized reward given to consumer in the B&C feedback loop is financially fulfilled at the point-of-sale using a virtual crediting system.

The consumer has now become a partner of the business, rather than a mere commercial object.

PART IV – Crediting System for Fulfilling Personalized Price Function

An important part of Sharener.com is a system used for fulfilling the personalized credits offered by the price function. Without such a fulfilling system, the personalized price function would be a mere theory without practical meaning.

The fulfillment system should be understood along with the payment system. As will be shown, the fulfillment system may be integrated with the payment system, but it may also be run in parallel to the payment system. The preferred fulfillment system is a virtual credit system as illustrated below.

To better explain the fulfillment system, the payment systems are first explained.

A. Background

A.1. Payment Systems

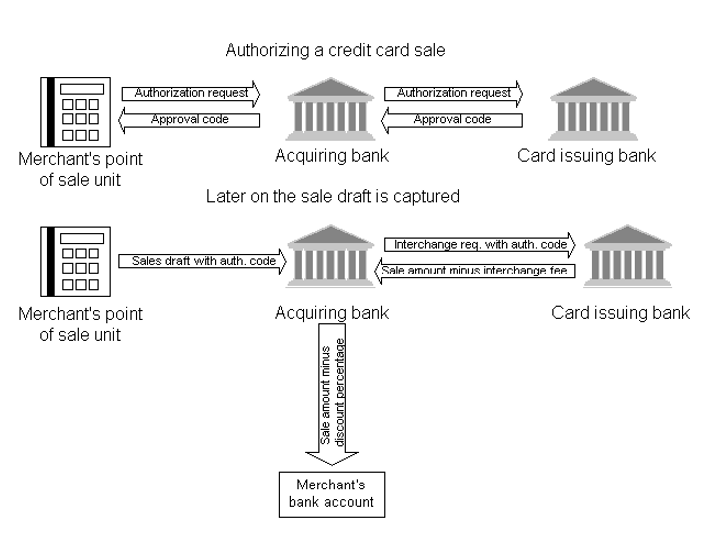

A.1.1. Traditional payment in retail:

A.1.2. A typical credit card payment process:

Problems with traditional credit card payment methods:

- Lack of security – requires buyer to provide credit card info by phone or mail to each business from which the consumer buys a product

- Lack of coverage – does not support transactions involving a party that is not set up for taking credit cards

- Lack of eligibility – not all potential buyers have or can get credit card

- Lack of support for microtransactions (micropayment)

A.1.3. Intermediary account payment method:

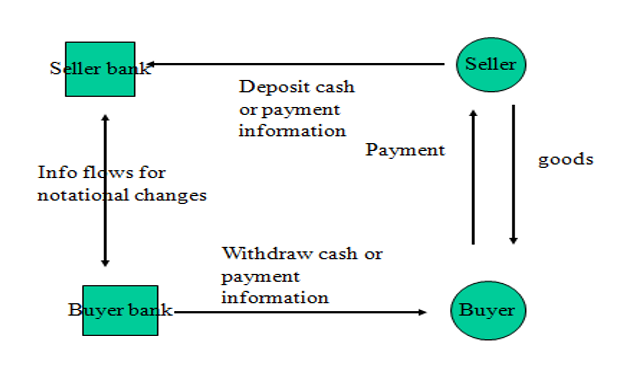

The Sharener platform may use any of the above payment systems. However, the focus of the Sharener platform is a system to fulfill the personalized credits, not the payment system itself. Whichever payment system is used, the selection may be made in his ability to facilitate the desired personalized credit fulfillment.Above is an illustration of an intermediary account payment method used by Alibaba.com on its B2C website Taobao.com. This method overcomes several problems that exist in the correctional payment methods.

A.2. Crediting methods for crediting buyer

- Coupon (very common)

- Rebate (not as common)

- Credit (rare)

- Cash (very rare)

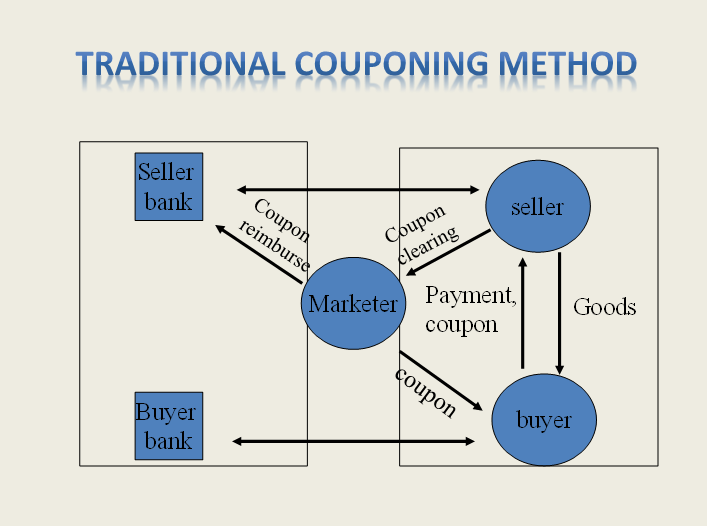

A.2.1. Traditional couponing method:

The concerns during the traditional couponing process:

- Marketer – most concerned of the following issues: (1) is the coupon used valid? (a matter of trust in the buyer) (2) is the underlying transaction valid? (a matter of trust in the seller). Whether or not the coupon transaction information received by the marketer for clearance can reliably answer the above two questions is critical in any couponing process.

- Seller – whether the marketer will honor the coupon that has already been redeemed by the seller at a retail point.

- Buyer – once the coupon is accepted and redeemed by the seller, the buyer has no more concerns.

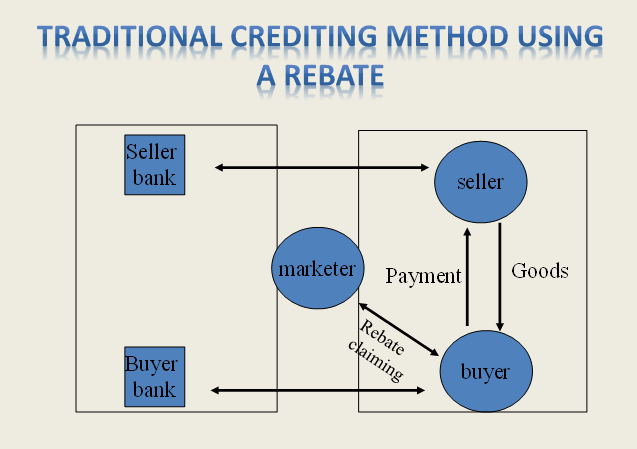

A.2.2. Traditional crediting method using a rebate:

The concerns during the rebate process:

- Marketer – (1) is the rebate used valid? (a matter of trust in the buyer); and (2) is the underlying transaction valid? (again a matter of trust in the buyer). Note that in the rebate process, the market has little reason to doubt about the seller.

- Seller – once the product has been sold to the seller, the seller has no more concerns.

- Buyer – whether the marketer will reimburse the rebate for the product that has been paid in full at a retail point.

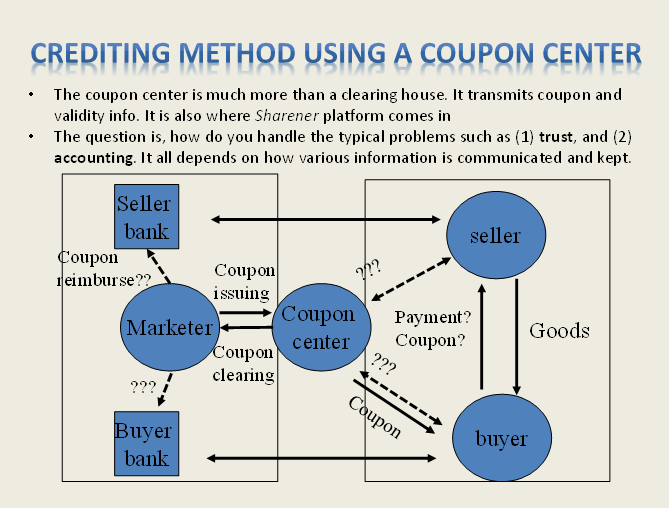

A.2.3. Crediting method using a coupon center:

Overview:

- The coupon center is much more than a clearing house. It transmits coupon and validity info. It is also where Sharener platform comes in

- The question is, how do you handle the typical problems such as (1) trust, and (2) accounting. It all depends on how various types of information is communicated and kept.

There are several optional models for implementing the crediting method using a coupon center:

Model One – Uses seller’s two-way communication equipment to accomplish coupon verification and clearing info transmission. This model is relatively difficult to implement at seller because the seller equipment needs to be integrated with POS to be able to transmit transaction information.

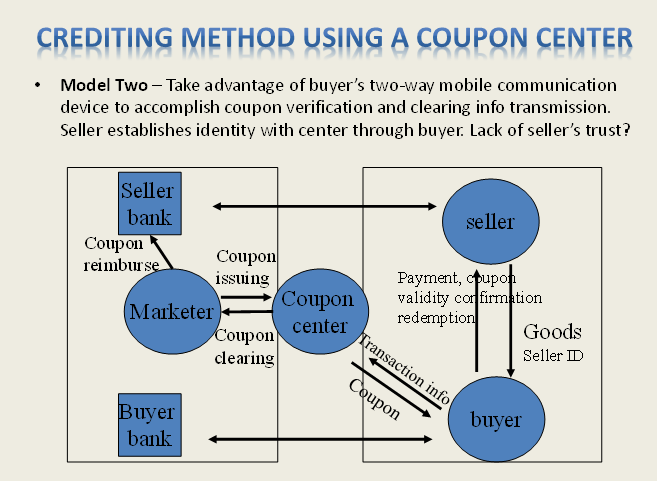

Model Two – Takes advantage of buyer’s two-way mobile communication device to accomplish coupon verification and clearing info transmission. Seller establishes identity with center through buyer. This model is easier to implement than Model One because it does not require special equipment at the retail point. However, there may be an issue of lack of seller’s trust in the buyer because the verification that goes through the buyer’s mobile convocation device may be a sham.

Furthermore, without anything connected to POS, there is an issue of who enters the transaction information such as purchase quantity and purchase price into the buyer’s mobile device in order to be transmitted to the coupon center. If the seller does, there is an extra burden on the cashier. If the buyer does, there is an issue of trust.

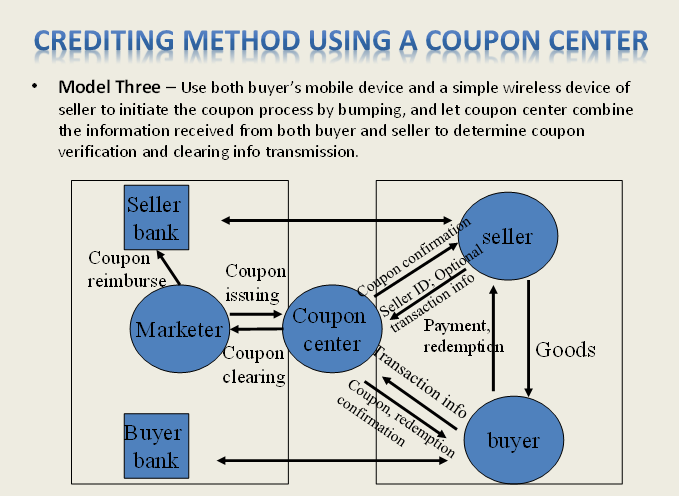

Model Three – Use both buyer’s mobile device and a simple wireless device of seller to initiate the coupon process by bumping the buyer’s mobile device against the seller’s wireless device, and let coupon center combine the information received from both buyer and seller to determine coupon verification and clearing info transmission.

Seller’s wireless device may transmit only the seller ID to the coupon center and does not have to transmit the transaction info. As a result, in the simplest form, Seller’s wireless device is not integrated with POS, nor does it communicate with the buyer’s mobile device in order to receive the transaction information.

At the same time, seller receives the coupon confirmation directly from the center rather than indirectly from the buyer’s mobile device like in Model Two. This may be more important than whether the buyer also receives the coupon confirmation from the coupon center, because the buyer has already received the discount, while the burden is on the seller to have the coupon cleared. In a rebate mode, the situation may be the opposite.

Likewise, without anything connected to POS, there is an issue of who enters the transaction information such as purchase quantity and purchase price into the buyer’s mobile device in order to be transmitted to the coupon center.

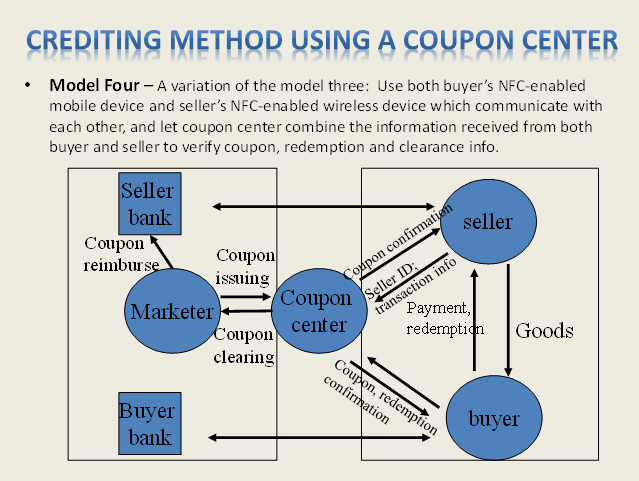

Model Four – A variation of the Model Three: Use both buyer’s NFC-enabled mobile device and seller’s NFC-enabled wireless device to communicate with each other, and let coupon center combine the information received from both buyer and seller to verify coupon, redemption and clearance info.

With Model Four, Seller’s wireless device may but does not have to be integrated with the POS like in Model One in order to obtain the transaction information and transmit the information to the coupon center. Instead, seller’s wireless device may receive the coupon information (and the associated information of the sold product) from the buyer’s mobile device.

At the same time, seller receives the coupon confirmation directly from the coupon center rather than indirectly from the buyer’s mobile device like in Model Two, resulting in a higher confidence of the seller in the coupon redemption.

B. The Problem

Sharener may use any of the above crediting methods as a part of its personalized credit fulfillment system. However, the crediting method may be further improved as disclosed herein.

One fundamental problem of using issued coupons to fulfill consumer pricing benefit is that unless the couponing process is integrated with the POS, it is difficult to communicate the exact purchase information to the coupon center (although it is relatively easy to communicate the coupon information to the coupon center to verify its validity).

Under the existing coupon systems, because the buyer pays a discounted price at the retail point, the burden is on the seller to verify and clear the coupon. The seller therefore would have an incentive to communicate the exact purchase information to the coupon center. However, unless the seller has proper equipment, it cannot do it easily. Besides, even if the seller is able to do so, it would be duplicating the data entry on the POS would a separate coupon system. Furthermore, even if the transaction information is communicated to the coupon center, it would be disconnected from the regular POS data entry. This would create difficulties in accounting and bookkeeping.

In addition to the information used for verifying the occurrence of the purchase, there is also a matter of the quantity of the purchase, and the price of the purchase. Such information is not easy to be entered and transmitted without integration with POS.

The key issue is therefore the proof for the sale, along with information for the quantity of the sale and the price of the purchase. The traditional way of accomplishing the proof is burdensome.

Under the coupon framework, what actually happens is that the marketer makes a conditional promise to the seller to compensate the discount the seller extended to the buyer. The condition for the payment is that an actual sale has he made using a valid coupon. In reality, the marketer holds the information for the validity of the coupon, and therefore is the most reasonable party to bear that part of the risk. To but the traditional couponing process asks the seller to bear that risk anyway, and is therefore not the most reasonable method.

On a more fundamental basis, in the traditional couponing process, the seller is playing a both a minus act (i.e., deducting the price at the point-of-sale) and a plus act (i.e., receiving compensation from the manufacturer) which are meant to cancel with each other eventually. This is fundamentally a superfluous requirement and unnecessary in a transparent space. Likewise, in traditional rebate process, the buyer is playing a similar and unnecessary two-step role.

Using proper tools an integrated commercial platform, Sharener may accomplish the same more easily and more reliably as discussed below.

C. The Solution

There may be multiple potential approaches for a solution.

Approach one – A straightforward solution is to connect the seller’s POS with the marketer through the intermediary coupon platform. But this is not the most desirable method because it requires heavy-duty implementation on the seller’s end.

Approach two – Another answer is to use a mobile payment system. If the buyer uses the mobile phone to pay for the product purchased at point-of-sale, connecting the buyer’s mobile phone with the intermediary coupon platform would be a very simple and reliable way to provide sale evidence, much like what the credit card system can do. If this design turns out to be prevailing, whoever owns the mobile payment system may also likely own the personalized credit system, or at least there needs to be very close collaboration between the owner of the mobile payment system and the owner of personalized credit system.

Approach three – Theoretically, the buyer may be required to submit physical evidence for purchase. But the solution is similar to rebate which is not only socially unacceptable, but is also very limited in use.

Approach four – Another option is to use a buyer identifier through the buyer’s mobile phone and an input of seller’s ID through the buyer’s mobile phone as a combined evidence for sale. This however has several disadvantages. First, the seller is left in dark because the buyer’s mobile phone could be displaying and sending false information. Second, it is difficult to enter sale quantity information. Asking the seller to enter the quantity information on the buyer’s mobile phone may be too much to ask. Third, even if the sale quantity information is entered, there is no check to verify its accuracy.

Approach five – A fairly robust but restrictive solution is OfferIQ’s approach based on a special credit card system.

- OfferIQ of Transactis integrates the coupon process with the POS.

- It does not require any special equipment at the seller’s end.

- Instead, it requires the buyer and the seller to join the platform, and also requires the buyer to make a purchase using a special credit card, whose transactions are accessible by the platform. This solves the problem of both accounting and the validity of the purchase.

- The problem is that it requires the buyer to use a special credit card to make a purchase. Other transactions including cash purchases will not work with offerIQ.

With OfferIQ’s system, the consumer becomes a member and is issued a special credit card to make purchases. The credit card system incorporates the coupon redemption and makes the payment and personalized crediting a single process. However, the solution has a limited scope due to his requirement of a credit card system. In countries like China and India, credit card use is not common and there is little indication that it would become common in the near future.

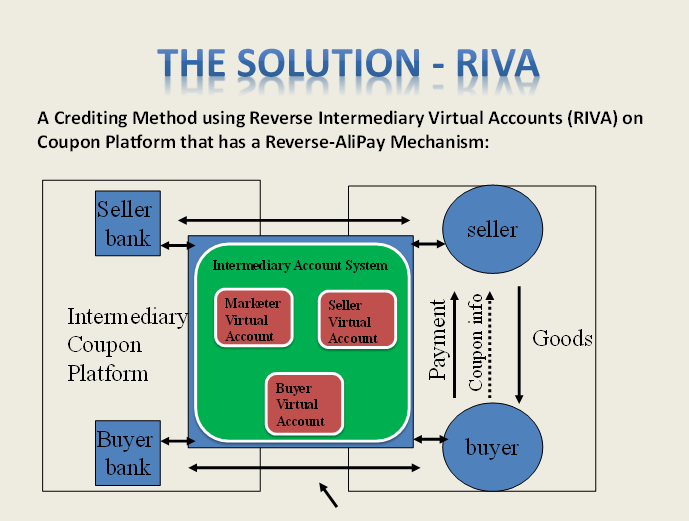

Approach Six – Reverse Intermediary Virtual Account (RIVA) system as disclosed herein is a more preferred solution. It may be especially suited for the countries like China and India, much like the AliPay payment model worked better in China than credit cards. In contrast to AliPay, RIVA operates in a reverse mode for personalized crediting (versus payment).

As a whole, unless an integrated mobile payment system is implemented, RIVA may be the best solution. Both the risk and the burden are balanced in RIVA, and there is a check on fraudulent acts.

Part V – RIVA Personalized Credit Fulfilling System

A preferred method for fulfilling personalized credits/incentives is Reverse Intermediary Virtual Account (RIVA) system disclosed herein. The RIVA system has a mechanism that is a reversal of AliPay virtual account mechanism. While AliPay is for a buyer to make a payment, RIVA is for a business platform to pay out a credit to the buyer.

The above illustrated Intermediary Account System constitutes a part of the personalized pricing fulfillment system in the business-consumer social networking system.

As will be illustrated below, RIVA system particularly suited for personalized pricing fulfillment.

The pricing of the product in a commercial world may be viewed as an approximation problem for the marketer to achieve the optimal price or “truth in price”. In this field, the regular price and is first-order approximation, while discounts, coupons, rebates, credits and personalized pricing can be generalized as second-order approximations. The RIVA system is primarily designed for “second-order pricing approximation” to realize personalized pricing, but may also be used as an integrated payment system including both the payments related to first-order pricing and the second-order pricing.

RIVA system is to do away with the conventional coupon and rebate methods. RIVA is a systematic personalized credit system.

RIVA is flexible and can be designed for optimized convenience and balance of risks among parties (the marketer, the seller, and the buyer).

RIVA to OfferIQ is analogous to what AliPay is to PayPal. Like AliPay, RIVA uses intermediary virtual accounts instead of credit cards. However, RIVA’s inventive mechanism is a reversal of AliPay.

There may be multiple modes in using the RIVA model as discussed below. It is noted that the different modes may be mixed on the platform. Even a single transaction may use a mixed mode in which one mode is used to fulfill a first part of the incentive/discount and another mode is used to fulfill the second part of the incentive/discount.

Mode One: the coupon mode

Step One: The platform determines a discount on a product for a consumer based on the personalized price function applied to the consumer.

Step Two: The platform presents the discount to the consumer.

Step Three: The consumer makes a purchase of the product at a seller that has joined the platform to honor the discount by presenting a coupon bearing the discount information, and pays a discounted amount to the seller. Preferably, the coupon is presented on a mobile phone of the consumer.

Step Four: When the Sharener platform determines that the consumer is making or has made a purchase, it notifies the marketer of the product about the purchase.

Step Five: The marketer of the product deposits a reimbursement value to cover the discount into the seller’s virtual account and optionally sends a notice of the deposit to the seller.

Step Six: After the marketer or the platform has received satisfactory proof of the purchase, the intermediary account system allows the deposited reimbursement value to be transferred to the seller’s bank (or another real financial account of the seller).

The above operation method, particularly Step Four for communicating purchase information to the platform, is further explained below.

One of the implementation keys is how the platform learns that the buyer is making or has made a purchase in the above step four. The platform system may learn about the consumer’s making a purchase in a variety of ways depending on the implementation of the fulfillment system.

In a first embodiment, the seller’s POS has network connection with Sharener platform and directly communicates the relevant information of the purchase event to the Sharener platform. However, such real-time communication between the POS and the platform is hardly necessary when Reverse Intermediary Virtual Account (RIVA) system is used. Alternatively, if a sufficient number of sellers have POS that can directly communicate with the platform in real-time, RIVA system may not be necessary, as the direct communication would provide sufficient proof for purchase in real-time for coupon clearance and therefore the “buffer” protection offered by RIVA may be unnecessary.

In a second embodiment, the seller’s POS has no direct connection with the Sharener platform, and the platform system receives the information of the purchase from separate means such as a cell phone of the customer.

Compared to the above first embodiment requiring POS networked with the platform, the second embodiment is much easier to implement. In this embodiment, the only thing the seller needs to do is to periodically send sale records to the platform for further proof of the sale (purchase) to complete the coupon clearance as indicated in the above step six. This may be done on a daily, weekly or even monthly basis, and is much easier than implementing a POS system capable of real-time communication with the platform. The platform may compare the records sent by the seller with the information received from the consumer’s mobile phone to verify the sale/purchase.

In a very simple implementation of the above second embodiment, the mobile phone of the consumer communicates the purchase information by sending a text message generated by the consumer manually. This can be done fairly conveniently and quickly using a specially designed mobile app installed on the mobile phone. Because the app can be designed to show linked information of the product being purchased, generating a text message with necessary information may be just a matter of a few clicks.

In a third embodiment, the retailer’s POS has no direct connection with the Sharener platform, and the platform system receives simultaneous and collaborating information of the purchase from the consumer’s mobile phone and a communication device of the seller.

Under the third embodiment, the seller may be equipped with a simple wireless device which is not necessarily connected to the POS. The seller’s wireless device transmits part of the sale event information. The buyer’s mobile phone transmits another part of the event information. The intermediary coupon system uses the combined information transmitted to determine both the validity of the coupon and the occurrence of a sale.

The seller may enter the purchase quantity information and the price on the seller’s side. Alternatively, the consumer (buyer) may enter such information by taking a photo of the purchase receipt.

One way to send simultaneous and collaborating information of purchase is to bump the consumer’s mobile phone with a wireless device of the seller. By way of using a sensor such as an accelerometer in the mobile phone and the communication device, the bumping causes each device to transmit simultaneous information of the purchase to the platform to be examined verified and stored. Become a dictation device of the seller may be another cell phone, where a specialty wireless communication device designed for such purpose.

Alternatively, the mobile phone of may communicate with the wireless device of the seller using NFC.

It may be assumed that each bumping represents a single unit purchase, and multiple bumpings represent a purchase of multiple units. However, the number of purchased units may also be entered by the seller manually.

However, due to the risk of seller/buyer entering a wrong quantity of units purchased (either mistakenly or intentionally), it may be necessary to require the seller periodically submit follow-up purchase information in order to clear the reimbursement deposited in the virtual account. This may be copies of physical receipts.

It is possible that multiple bumping may prove to be too difficult to manage. In that case, it may be necessary to limit the purchase to a single unit for each buyer each day. This would limit the use of the system, but increase the robustness and simplicity of the system.

Compared to the first embodiment requiring POS networked with the platform, this third embodiment is still much easier to implement, although it may be more difficult than the above second embodiment. However, compared to the above second embodiment, the third embodiment may have several advantages. First, it may have a strong enough one-time simultaneous and collaborative information of the purchase to verify the purchase for the purpose of coupon clearance, and therefore there may be no need for the seller to submit additional evidence to prove the purchase. Furthermore, selective or random auditing helps to further reduce fraud. Second, on a fundamental basis, the above third embodiment has a distributed and more balanced burden sharing among the parties, potentially an improvement over the traditional coupon mode or rebate mode that has skewed shift of burdens.

Mode Two: the rebate mode

Step One: The platform determines a discount on a product for a consumer based on the personalized price function applied to the consumer.

Step Two: The platform presents the discount to the consumer.

Step Three: The consumer makes a purchase of the product at a seller, and pays the full amount to the seller.

Step Four: When the Sharener platform determines that the consumer is making or has made a purchase, it notifies the marketer of the product about the purchase.

Step Five: The marketer of the product deposits a reimbursement value to cover the discount into the consumer’s (buyer’s) virtual account and optionally sends a notice of the deposit to the buyer.

Step Six: After the marketer or the platform has received satisfactory proof of the purchase, the intermediary account system allows the deposited reimbursement value to be transferred to the consumer’s bank (or another real financial account of the consumer).

Like that in mode one (the coupon mode), one of the implementation keys is to let the platform determine that the consumer is making or has made a purchase. The several exemplary embodiments discussed above may be used here as well. But it is noted that because the burden of proof in the rebate mode is different from that in the coupon mode, the implementation details and priorities may be different.

Most notably, under the rebate mode the consumer has a strong incentive to provide the evidence for proof because the consumer has tentatively paid a full amount and may receive reimbursement only upon the platform’s receiving the satisfactory evidence. For this reason, it may be possible in the rebate mode to leave the seller completely outside of the rebate loop. This has an advantage of not requiring any retailer involvement in the personalized discount or crediting process at all. The retailer sells the product and receives the payment as if the consumer is making a regular purchase.

However, such implementation may risk suffering consumer fraud. Nevertheless, the following characteristics of Sharener help mitigate the risk of fraud. (1) the Sharener platform is a real identity-based community; (2) the consumer’s cell phone is registered with the platform and serves as a physical ID of the consumer when used to facilitate the purchase; (3) each consumer has a financial stake in maintaining and improving a good social status on the platform; and (4) because the level of discount received by the consumer increases as the social status of consumer becomes higher, the larger the amount subject to fraud is, the greater is the financial statement of the consumer. When these factors are in place, the fraud rate may be expected to be within the tolerable limits.

Furthermore, selective or random auditing helps to further reduce frauds. An audit may require the consumer to submit a purchase receipt and/or a cut-off barcode of the product packaging. The selective or random auditing may be performed immediately upon purchase and without prewarning. This way, there’s no risk that the consumer may have lost the receipt or the product packaging by the time a selective or random auditing is notified. The rate of calling selective or random auditing can be a very small percentage (e.g., 1%, or .1%) of all purchases, and the rate may be variable from product to product and time to time. The system may determine an optimal rate based on the past data.

Unlike traditional rebate process that requires submitting various physical purchase evidence, the buyer may just simply submit a scan or photo of the receipt taken by the mobile phone. This is a much easier process than the traditional rebate.

Mode Three: the mixed mode

Step One: The consumer obtains a first discount on a product. The first discount may be provided by any source, even outside of the platform, and can be any type of discount.

The platform determines a second discount on the product for the consumer based on the personalized price function applied to the consumer. The second discount is separate from the first discount but applicable to the same product.

Step Two: The platform presents the second discount to the consumer.

Step Three: The consumer makes a purchase of the product at a seller, and pays a discounted price, which is the full amount minus the first discount, to the seller.

Step Four: When the Sharener platform determines that the consumer is making or has made a purchase, it notifies the marketer of the product about the purchase.

Step Five: The marketer of the product deposits a reimbursement value to cover the second discount into the consumer’s (buyer’s) virtual account and optionally sends a notice of the deposit to the buyer.

Step Six: After the marketer or the platform has received satisfactory proof of the purchase, the intermediary account system allows the deposited reimbursement value to be transferred to the consumer’s bank (or another real financial account of the consumer).

In the above mixed mode, the consumer first receives a regular discount at the seller. This part may be done in connection with the platform, but may also be done outside of the platform in the same way as any consumer who is not a member of the platform does. But if the consumer is also a platform member, he may enjoy the benefit of a second discount offered and fulfilled by the platform.

Mode Four: the credit-earning mode

If the consumer has not earned a personal discount on the product to be purchased, he may still use a credit-earning mode to purchase the product to establish personal credit effective in the personalized price function. In the following credit-earning mode, an un-earned discount is optional.

Step One: The consumer obtains an unearned discount on a product. The discount may be provided by any source, even outside of the platform, and can be any type of discount.

Step Two: The platform establishes a link to the product for the consumer, and presents the link to the consumer. This may be either pushed to the consumer by the platform, or pulled by the consumer from the platform.

Step Three: The consumer makes a purchase of the product at a seller, and pays a discounted price with the unearned discount, to the seller.

Step Four: When the platform determines that the consumer is making or has made a purchase, it updates the personal profile of the consumer.

It is noted that in the above described operation mode, there is no restriction as to how the consumer makes the payment. Where no POS integration with the Sharener platform is required, there is no restriction as to where the consumer shops (online or off-line, retailer registered with Sharener or not, etc.).

However, purchases made by certain special consumer groups may be with particular attention.

The first example is purchases made by customers using a credit card. In this case, the purchase proof may be obtained by the platform from the credit card company (credit card processor) which has credit card payment transaction records. Due to the advantageous use of the virtual account system, there is no need to have real-time communication with the credit card company. Instead, the platform only needs to receive a copy of the accumulated records periodically for cardholders who are members of Sharener. This is much less burdensome as compared to the full-scale credit card payment system integration required by prior art systems. As the Sharener platform can recommend its customers to apply for a new credit card, this collaboration between the Sharener and the credit card company is mutually attractive.

The second example is purchases made by consumers using a mobile phone payment method. Like that with credit card payment, the purchase proof may be obtained by the platform from the wireless carrier, and the deliverance of the information may only need to be done selectively and periodically and does not require real-time communication nor deep integration. Because the Sharener platform helps to enhance the usage of mobile payment, the collaboration between the Sharener and the wireless carrier is mutually attractive.

In either of the above examples, the rebate mode is preferred as it does not require any retailer involvement, but any other mode may also be used.

It is further noted that, although the above descriptions make a distinction between “marketer” and “seller”, in certain circumstances the marketer and the seller may be either identical or directly affiliated. For example, a local restaurant may be both the marketer and the seller in relation to the Sharener platform.

PART VI – Purchase Proof Based on Code-Verification

Unless the seller’s POS is connected to platform, the platform may require that the consumer send the proof for purchase in order to receive the benefit offered by the platform. One simple way is to let the consumer self-report, subject to selective or random auditing. The self-report can be as simple as a click linked to the product, or a text message linked to the product. The purchase proof may be a digital scan of the purchase receipt, a digital scan of the product packaging (e.g., barcode), or mail-in physical evidence. Digital scans may be done at the time of the purchase using a mobile phone.

Disclosed herein is a novel method for purchase proof based on code-verification.

The product manufacturer places a product code on the product. After the Sharener consumer has purchased the product, the consumer sends the product code (optionally along with other information related to the purchase) to a verification center associated with the platform as evidence of purchase.

The product code verification center may either be a part of the Sharener platform or a third party service platform which communicates with the Sharener platform.

Any one or a number of the following measures may be used to enhance the security and reliability of the verification process.

In one embodiment, the product code includes a product identification code that uniquely identifies the particular unit of the product being purchased. The verification center maintains records of the product identification code and the records of the instances of verification. The center may allow only a one-time verification for each unique product identification code.

In another embodiment, the product code includes a concealed code (e.g., covered by a scratch-off material, hidden inside a packaging), which can be revealed by the consumer upon purchasing the product.

In another embodiment, the product code is a combination of the both an overt product identification code and covert verification code, as disclosed in US patent Applications No. 13079022, No. 13079024, and No. 13118605, all entitled “ANTI-COUNTERFEITING MARKING WITH ASYMMETRICAL CONCEALMENT”, which applications are fully incorporation herein.

An exemplary procedure of verification method is as follows:

(1) associating a first code with an article, the first code being able to identify the article at a desired level of specificity;

(2) associating a second code with the first code as a confirmation code to verify the first code;

(3) reproducing the first code and the second code on or in the article, the first code being overt to normal viewing, and the second code being covert from normal viewing and is only conditionally revealed;

(4) receiving the first code and the second code at a verification center;

(5) comparing the received first code with article code records stored in the data storage to identify the product; and

(6) verifying that the article has been purchased by matching the second code received and the second code found in the article code records in association with the first code.

Typically, the article is placed in a retail channel which eventually sells the article to a consumer who reveals the second code and sends both the first code and the second code to the verification center for verification.

The second code is preferably covered with a means which is invasively removable. That is, the covert means can be removed only with certain damage, and once removed it cannot be easily recovered. One example of such invasively removable means is a scratch off material.

The first code may be an alphanumerical code, a barcode, a 2-D code, or RFID.

The consumer may send the product code for verification in a variety of ways. One simple method is to call the verification center which is linked to the Sharener platform. Another way is a send a text message that contains the code. In one The product code verification may be an integral part of a Sharener App installed on the mobile phone of the consumer. The App maintains an identified connection with the platform and automatically links the consumer’s user account, product identification and verification code together.

With the above code-verification method, a Sharener consumer may need no further evidence to prove purchase.

Because the above method can also be used for anti-counterfeiting, it may have a double attraction to the manufacturers, as well as a double attraction to consumers.

In one operation mode, the verification center is part of the Sharener.com platform. When the consumer sends in the production codes, the verification center makes verification and confirms the purchase in real time.

In another operation mode, the verification center is a third-party service center in collaboration with Sharener.com platform. For example, the verification center may be anti-counterfeiting center whose main function is for anticounterfeiting. The anticounterfeiting center is in communication with Sharener.com to send the verification results to Sharener.com. The communication may either be in real time for every event of verification, but may also be done periodically (e.g. weekly, or monthly) with cumulative reports.

PART VII – Sharener and “the Internet of Things”

Using the Internet of Things, traditional advertising media can be connected to Sharener platform to make consumers’ viewing the advertisement trackable, and such tracked information may be used as a parameter in the price function to influence the personalized price of the consumer.

For example, any visible advertisement (printed materials, posters and bulletin boards) may bear a machine-readable code (such as a 2-D code). When the consumer sees the advertisement, he uses his mobile phone to scope the advertisement to read the code. The code read by the mobile phone is sent to Sharener platform (along with other information such as the consumer’s account identification information or the cell phone number), where the code is automatically registered and identified at the Sharener platform in association with the respective business, a type of products, or a particular product to indicate a count of advertisement viewing.

Because the code identifies the product or the brand, the registered viewing may automatically contribute to the viewer’s personal profile in relation to the product or the brand to effectuate a favorable factor in the viewer’s the personalized price. Because the viewing data is connected to the viewer’s other consumer behavior (e.g., making a purchase), it serves as a rich source for analyzing advertisement viewership and effectiveness.

The same can be done on any object bearing a machine-readable code. In addition to active advertisements, the object bearing machine-readable code may be a product packaging. A counted view of the object may be given a different score depending on the type of the object that is being viewed. Viewing of certain objects may result in a contribution to a higher score which influences the personalized price, while viewing of some other objects may not result in such a contribution, but instead is just used for the consumer to connect to a product or brand automatically through the central website.

The result: a transparent relational space and advertising space between consumers and businesses.

One significant potential benefit of extending Sharener to the Internet of Things is that the advertisement space may suddenly become transparent to the advertiser. With conventional advertisements, it is generally difficult for the advertiser to gauge an accurate viewership, and even more difficult to measure the response to the advertisements. When linked to the Sharener platform through the Internet of Things, the accurately registered ad view accounts plus any statistically identifiable changes in the consumer behavior would make both the viewership and the response to the advertisement quantifiable and accurately measurable.

Therefore, when Sharener platform incorporates “Internet of Things”, and uses embedded codes to convert physical objects (things) to “clickable links”, it creates layers of new applications not found on the ordinary “Internet of Things”.

There are several differences between this invention and the ordinary “Internet of Things”.

First, in the “Internet of Things”, each code carried by an object corresponds to and leads to a URL on the Internet to show information, while in the present invention, the code may or may not correspond to and lead to a URL. It only needs to be associated with and be able to identify a certain brand, a business, or a product was submitted to the centralized platform Sharener.com. Such association may be done using a unique URL, and therefore any object in the ordinary “Internet of Things” naturally becomes part of the extended Sharener platform for the above purpose. However, such association may be prearranged by the business in coordination with Sharener.com, and in this way the code needs not to be a URL but can be any code that gives a sufficient basis for brand and/or product identification on the Sharener platform. In this sense, the extended Sharener platform according to this invention is broader than the “Internet of things” in scope regardless of function.

Second, the extended Sharener.com operates in a different way compared to the “Internet of Things”. While the “Internet of Things” connects various objects to various websites and URLs, the extended Sharener platform always connects to a centralized platform Sharener.com where the brand and product association with the information is performed, stored, analyzed and used.